Diagnosing Early-stage Capital Gaps and the Importance of Weak Signals

A report on North American and European university VC funds supports NACO's recent report that identifies a significant pre-seed funding gap for innovative Canadian startups

A recent study of what the authors call “university venture capital” (UVC) in North American and Europe provides an interesting point of convergence for several threads that have been floating around the innovation ecosystem over the past several weeks. Before reading the rest of this article, I suggest at least skimming “University venture capital in Europe and North America: Evidence, models, and EU policy implications”, an article by Thomas Crispeels, Emiel De Buyser, James P. Gavigan, and Ramón Compañó. This work contains a wealth of data and policy insights from across a large subset of OECD countries, and is well worth a read on its own.

They frame the problem clearly:

“[University spin-offs (USO)s] often encounter significant barriers in accessing early-stage investments by Business Angels and Venture Capitalists (VC). Their dependence on intangible assets, early-stage technologies, and the absence of a commercial track record make it difficult for investors to evaluate their viability. This information asymmetry leads to a persistent funding gap, as traditional VC firms tend to favour more mature ventures with clearer market potential.”

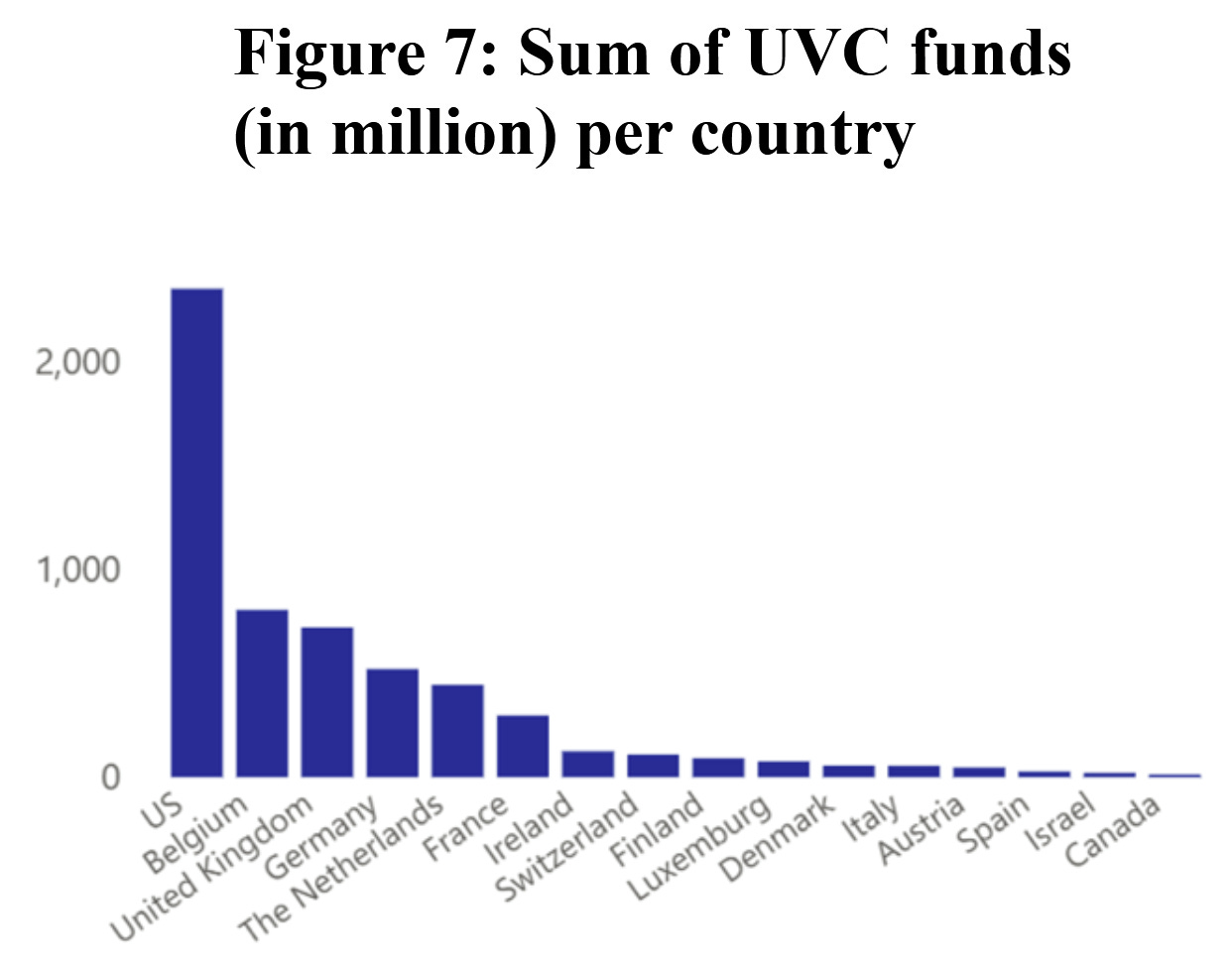

The results strongly support a recent report by the National Angel Capital Association (NACO) that demonstrated that Canada is missing 141M and $181M USD in pre-seed and seed-stage investment capital, respectively, relative to the United States, resulting in $66B in foregone economic value creation. Contributing to that gap, Crispeels et al. show, is that Canada sits in last place for total UVC among countries surveyed (see Figure 7, reproduced below).

This total number hides a heterogeneous domestic UVC landscape. Several Canadian universities have investment arms that are of a size consistent with the global medians in terms of total assets under management, as discussed in detail in my article covering such funds. Acknowledging the existence and importance of those outliers, the fact remains that Canada lags the world in this area, a problem I believe is foundational to our lagging productivity in general. A careful read of this work, informed by the recently published simulation model on effective investment strategies for emerging technology, offers clues as to structural reasons for the gap.

In this article, I connect the dots between this paper, my recent simulations of venture philanthropy, my survey of Canadian university deep tech funds, NACO’s findings of missing Canadian early-stage capital, and several university-related topics about which I have written in the past. Combined with NACO’s report, this work is confirmation of several “weak signals” that I have been writing about for some time, and a call to action for Canada both to address these gaps and to commit to collecting the data needed to be able to proactively identify them in the future.

Weak signals

Innovation arises as the result of accurately identifying and acting early on weak signals of impending change. One such signal exists in this paper, as well as in my own previous research on the topic: Crispeels et al. observe a trend toward larger and larger structures in a small but growing minority of UVC funds:

“[W]e observe that the amount of UVC available in Europe is growing, with some notable trends: the emergence of multi-university UVCs attracting larger investments, the occurrence of international multi-university UVCs, and the evolution towards a broader investment scope (e.g., investing in companies that collaborate with universities or in-license university intellectual property rights).”

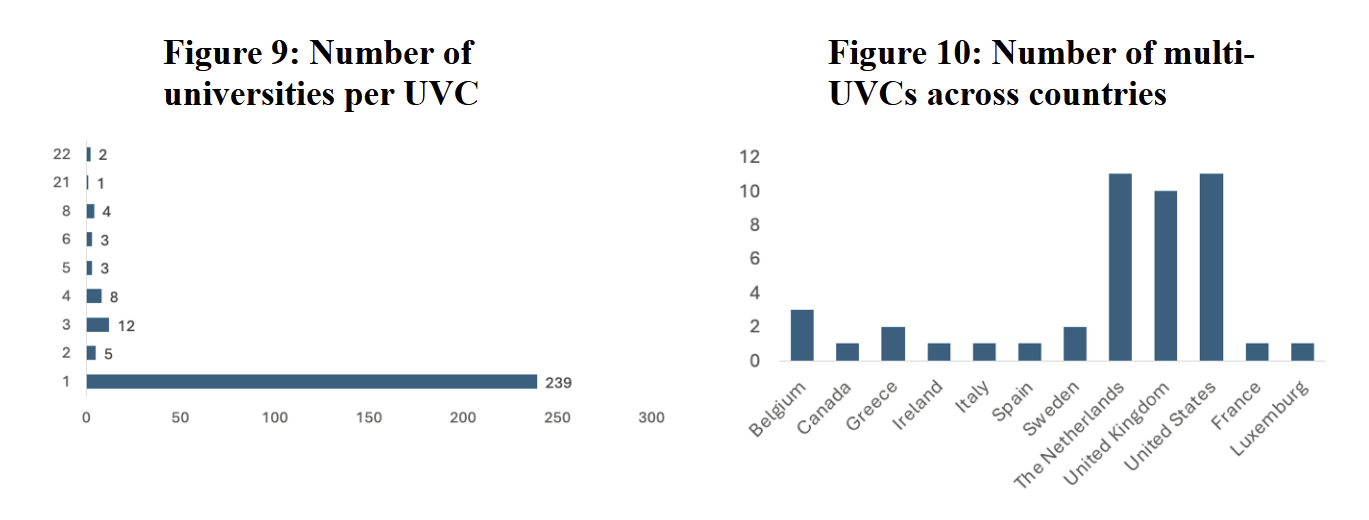

Figures 9 and 10 in particular, reproduced below, show a small but growing minority of multi-university investment funds. It appears that several universities, across Europe in particular, are pooling their investment resources.

As I was conducting the interviews for my previous article, it came quickly clear that in cases where universities had iterated at least once in terms of their approach, the second attempt usually involved an entity that was at a greater structural distance from the university, and that had an expanded investment scope, as compared to the first.

By way of example, the fund with the longest track record that I surveyed (Velocity Fund in Waterloo) has actually gone through several iterations, ending up with an almost entirely separate entity from the university (the university is an LP in the latest fund) that invests globally. UCeed in Calgary, (built and led by John Wilson, who previously had a hand in building the UK approach), is managed by a wholly-owned but arm’s-length subsidiary of the university, and has a provincial scope for some of its sub-funds. While not a multi-university approach in most cases, the trend toward larger and larger investment scope is the same.

Scale matters

In light of recent results from simulations of investment in university-affiliated companies, this trend should not be all that surprising. The key takeaway from that work was that the single most important determinant of long-term success is scale. Where emerging technology is concerned, it is more important to make sure that you do not miss the homeruns than it is to ensure success with every investment - median returns are dictated entirely by the presence of outliers in your portfolio. Combined with the fact that it is all but impossible to predict which attempts to commercialize research will be successful at the founding stage, and it becomes clear that UVC, like any emerging technology investment play, is primarily a numbers game. Seen through this lens, the trend toward larger and larger investment scope that we are seeing in Canada, and the trend toward multi-institution and even cross-border UVC funds in Europe, makes perfect sense.

Canadian universities are at a crossroads, with recent shifts in policy applying pressure toward delivering the “third mission” of universities to demonstrate direct societal impact (and specifically, economic impact) of their research. All of these pieces of evidence point in the same direction: a broadly scoped fund with pooled resources can make more investments, while most single universities alone will struggle to achieve the necessary scale through no fault of their own.

There is a subtle nuance here that is worth spelling out. While the combined effect of many disconnected UVC funds would be the same at the ecosystem level as a pooled fund of the same total size, individually those 10 disconnected funds will experience extreme variance and will individually perform very differently, with some succeeding and some failing, exposing individual institutions to a much higher degree of risk and jeopardizing the long-term impact of the while enterprise some universities drop off, leaving their spinouts without support and driving a heterogeneous landscape of research commercialization effectiveness. A larger, combined fund approach serves both to smooth out this variance, both geographically and at the level of fund performance, to increase the median investment performance, and thereby reduces individual university risk exposure.

The lessons for Canada

This tendency toward consolidated UVC is rational. It is reflected in a recommendation also made by the European Commission. As noted by Crispeels et al.:

“The European Commission […] contains a number of measures to boost the creation of innovative firms in the EU, targeting universities. One measure refers to support cross-border networking and collaboration between leading hubs rooted in strong university ecosystems.”

Of course, this is not the whole story. If emerging technology and research commercialization is a numbers game, then dealflow is critical, and the lack of focus on UVC in Canada also reflects a “chicken and egg” problem, wherein researcher-led entrepreneurship is not necessarily built into the culture of all Canadian universities (though there are some obvious exceptions), resulting in lower dealflow that in turns reinforces the difficulty involved in building effective single-institutions funds. This vicious cycle is examined through different lenses in my article on the importance of embracing risk in early-stage innovation, as well as on embedding entrepreneurial culture in university faculty. The European Commission also addresses this issue:

“A second [measure recommended by the European Commission] is to develop a blueprint for an academic career development framework that rewards research commercialisation [sic] activities, including considering staff mobility between the university and industry in academic staff evaluation and promotion criteria. Rewarding faculty members involved in the commercialization of research results and spin-off creation increases their propensity to contribute more to spin-off formation and knowledge transfer activity.”

The PTIE movement in the United States, which is readily adaptable to Canada, gives us a concrete roadmap for addressing this point.

While great progress has been made in several Canadian regional and provincial ecosystems with respect to university spinout investment, there remains an enormous amount of Canadian research that lacks reliable pre-seed funding for commercialization, as evidenced both by this paper and NACO’s findings.

Canada has a lot to learn from our European allies, and the findings of this paper will be an important consideration as Canadian universities (and Canada generally) responds to the early-stage capital gap and to shifting societal expectations of its universities. The important takeaway from the point of view of the broader Canadian innovation ecosystem is that weak signals are critical to getting ahead of global trends, and detecting them is impossible if we are not collecting and critically evaluating data on our innovation performance, at every level.

As we enact sweeping changes to our approach to innovation, now more than ever Canada needs to make collection and coordinated analysis of effective, long-term performance metrics a matter of course across all levels of our innovation ecosystem. This will enable us to detect these weak signals early so that we can proactively address gaps, rather than react to their revelation after the damage is done and the signal is no longer weak.

Yes, this is getting to the heart of the matter. It really may be more of a ‘spray and pray’ approach at that stage. I think regenerative fund models make a lot of sense where eventual returns are reinvested in the system itself that propagates more innovation.

I hesitate to call it a university fund though, because these funds are largely the actual foundations of positive societal change - it is investing in our own advancement collectively, and isolating it to universities makes it sound like a niche project. (Just a thought to consider)..